Balpeng

The balloon-model (Enstam, 1995, 26pp) was, as we have mentioned before, developed to structure and visualise problems that are difficult to measure in business economy terms. It has primarily been used in the field of human resources but is also applicable to other areas. The model is presented out of a business perspective. This implies that the focus is upon the consequences for the business operations.

The model is based on seven chronological phases. They are:

1. Identify the problem.

Give a detailed description of the problem area.

2. Describe the different alternatives of action.

Are there different alternatives, which should be investigated further? To be able to identify the consequences of the action, it has to be compared with some other alternative situation. In this stage you decide which alternative situation that should be used for comparison.

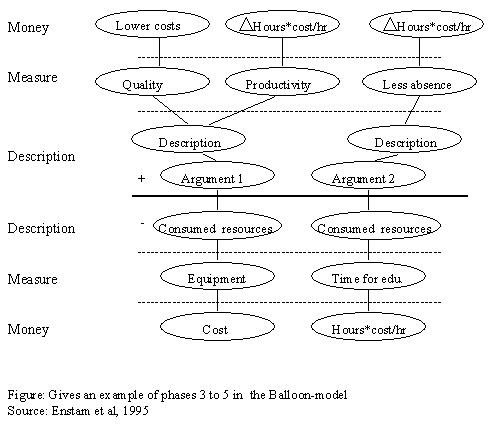

3. Describe the consequences of the action.

What are the implications on business operations from this action? The positive effects are written in balloons over a drawn line meanwhile the negative effects are drawn below the line, hence the balloon-model (see figure below).

4. Quantify the consequences.

How can the consequences be quantified in units? If it is possible, this is done in this phase.

5. Give a monetary value to the quantified consequences.

6. Make an investment calculation.

The consequences of an action of have long term effects on operations. It is therefore reasonable to make an investment calculation.

7. Make a sensitivity analysis of the calculation.

Since the calculation is built on estimates, it would be interesting to see how sensitive the calculation is to changes.

PENG (Dahlgren et al, 1997, 33pp) stands for Prioritering Efter NyttoGrunder and was developed to aid decision

support in IT-investments by identifying and measuring the benefits of an IT-investment. The method for doing this is a 10 step process:

1. Determine the purpose.

Possible purposes can be to decide whether an investment should be carried out or not. Another purpose could be decision support for price setting.

2. Involvement.

Often the full potential of an IT-investment is not accomplished because of the lack of involvement from all concerned parts. In this phase all people involved in the project should be informed of the goals and implications of the evaluation project.

3. Choose area of investigation.

Which part of the company is to be studied? Depending on the purpose of the investigation a starting point should be used for the evaluation. For an IT-investment it could be the companies working processes or information systems.

4. Define and describe the processes/systems.

In order to be able to make a successful benefit evaluation it is necessary to study the current processes/systems. Different techniques can be used to describe the processes/systems but they lie outside the scope of the PENG-model. These techniques can, for example, include using existing quality documentation like manuals or other technical documentation to describe the existing systems.

5. Identify the effects of the benefits.

In this phase persons that are affected by the investment should be involved. Some processes involve people outside the own organisation, like customers and suppliers. If the actors outside the organisation can be involved this strengthens the results of the evaluation.

6. Link the benefits of the investment to the main goal.

All benefit effects aim at either directly or indirectly fulfilling the goals of the investment. Therefore, one should in this phase, relate the benefit effects to the main goal. This makes it possible to rank the benefits on the basis of their contribution to the main goal.

7. Define the value of the benefit.

This step includes deciding for which period of time the investment should be evaluated. Also, all benefits do not necessarily increase income or lower costs, some may for example keep market share constant, when they would have been lost without the investment.

8. Estimate the reliability of the evaluation.

This is done by categorising the benefits in three different classes. Direct benefits, indirect benefits and intangible benefits. This is done to see the proportions of the categories which in turn gives an estimate on how reliable the investment is. This phase includes a validation process where the results of the evaluation are compared in order

to see whether the same benefit has been included twice and to see that the total sum of the benefits appeared to be realistic.

9. Define and estimate the IT costs.

Like the benefits the costs can be categorised. Central costs, local visible costs and local hidden costs. Local hidden costs are those that are most difficult to identify, they often include staff costs, for example IT support within the own organisation.

10. Calculate net benefits.

Compare the value of the benefits to the costs of the investment.

Please switch to the main text web browser window to continue reading.